Equity-Backed Loans for Founders: Risks, Trade-Offs, and Diversification Alternatives

Many founders reach a point where their net worth is concentrated in paper wealth.

They may be worth tens or even hundreds of millions of dollars, but most of that wealth is tied up in illiquid private shares of their startup¹⁰. Equity they can’t liquidate easily. This is a recurring issue among founders who have a significant share of their personal net worth concentrated in private company equity¹¹.

So what should founders do when they need liquidity? Or, more fundamentally, what should they do to reduce their concentration risk?¹²

One common route is secondary sales. But if the founder believes in the upside of their company and doesn't want to give up that potential, another option is equity-backed loans1.

What Are Equity-Backed Loans?

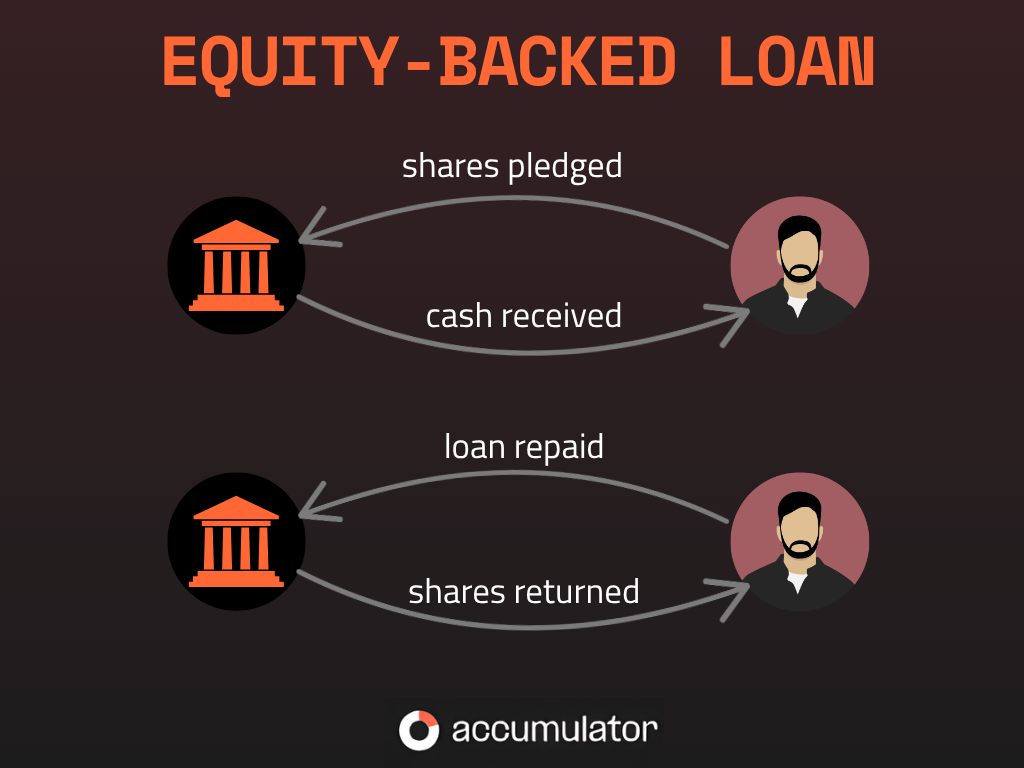

An equity-backed loan is a form of financing where founders or early employees borrow money using their private company shares as collateral1.

Instead of selling equity in a secondary market, the borrower pledges their shares to a lender. In return, the lender provides a loan that must be repaid over time, typically with interest.

Basic Structure1

Here’s how the basic structure of an equity-backed loan looks:

- The borrower pledges startup shares as collateral.

- The lender evaluates the value and risk profile of those shares.

- The lender determines the loan terms, including the amount, interest rate, and collateral required.

- The borrower receives cash and repays the loan according to the agreed terms.

If the borrower repays the loan successfully, the pledged shares are returned. If, on the other hand, the borrower defaults, the lender may have rights to the collateralized shares.

Key Features

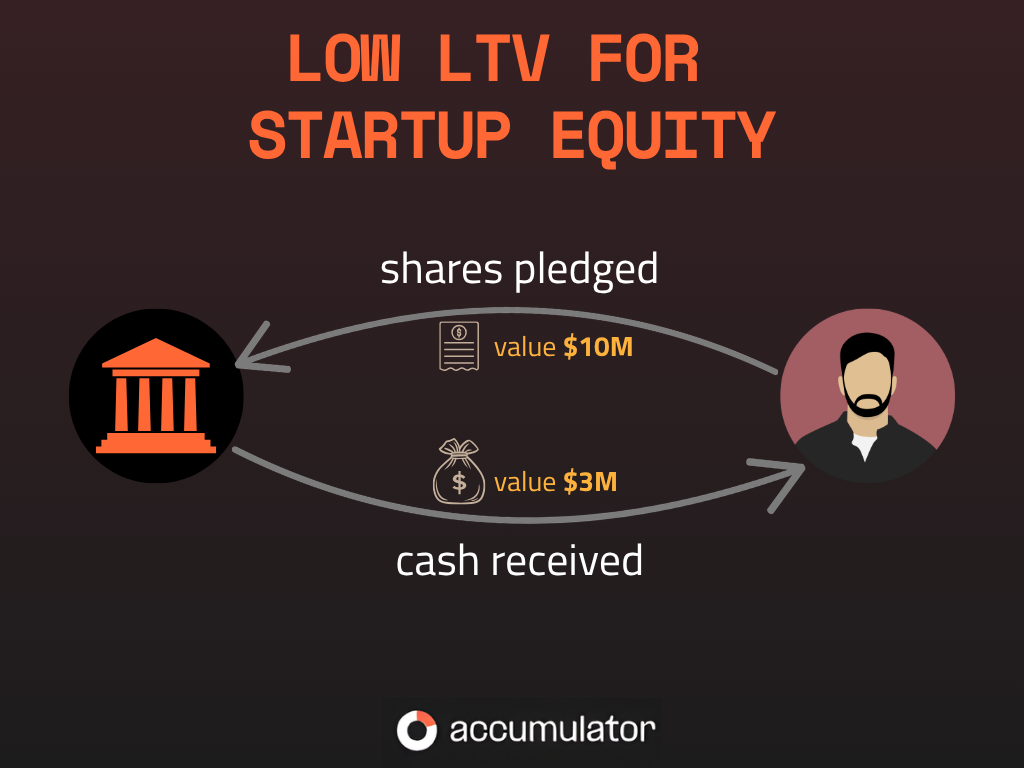

Lenders structure equity-backed loans conservatively since startup shares are deemed risky. These shares are difficult to sell, their valuations change quickly, and liquidity events are unpredictable¹³.

So, the typical loan-to-value ratio (LTV) for startup equity is quite low, often around 30%2. Meaning, founders receive only $3M for a $10M value of shares.2

Interest rates on equity-backed loans are also generally higher than traditional loans and can reach up to 15% annually.2

One advantage here is that many equity-backed loans are structured as non-recourse. In case of defaults, the lender can only seize the pledged shares and cannot pursue the borrower’s personal assets or income.

On the flip side, these loans often come with additional charges that may not be obvious at the outset. The origination fees, platform fees, cashout fees may not look significant individually, but when added up with the interest payable, the effective annual cost can reach 20% in some cases.2

Major Providers of Equity-Backed Loans

Several companies have built specialized businesses around lending to founders and employees of private companies.

Here are selected companies operating in the market:

Quid

Quid focuses on late-stage startups approaching IPO.

The loan structure is marketed as non-recourse, meaning borrowers are not personally liable if the company fails and the shares become worthless.

The company has provided financing to shareholders at companies including Airbnb, Uber, Lyft, Palantir, and Flexport.

The company emphasizes speed, claiming transactions can close within 36 hours of signing a term sheet compared to months for a secondary sale.

Secfi

Secfi provides financing and wealth management services. The company also offers secondary sales along with security-backed loans. It positions itself as a broader equity management platform.

Secfi’s financing structure includes a 5% platform fee, an advance rate similar to interest, and an equity share based on the stock's exit value. Again, it’s a non-recourse financing.

Secfi’s clients include employees from DoorDash, Reddit, SeatGeek, Palantir, Netskope, and Upgrade.

Liquid Stock

Liquid Stock offers non-recourse financing for option exercises and shareholder liquidity.

Liquid Stock describes itself as a fully independent, institutionally backed investment firm focused on providing liquidity to employees and shareholders of privately held pre-IPO companies.

The company also offers financing for option holders and secondary sale for shareholders. Notable clients include shareholders and option holders from Airbnb, DocuSign, and Uber.

Other providers

There are lots of other companies that operate in adjacent spaces or offer similar products.

Even traditional and private banks occasionally offer lending products secured by private company shares, though these are typically available only to high-net-worth clients with broader banking relationships.

What Equity-Backed Loans Solve Well, and What They Don't

Since almost all founders have most of their net worth concentrated in a single asset, the main goal is diversification, or reducing concentration risk¹⁴.

With that in mind, here's what equity-backed loans do and don't address.

What Equity-Backed Loans Solve Well

- Access to liquidity without selling shares: The most obvious benefit. Founders retain their shares and benefit from any future upside in the company’s valuation.

- No immediate taxable event: Borrowing against shares generally may not be treated as a sale for capital-gains purposes9.

- Non-recourse structures limit personal liability: Most equity-backed loans are non-recourse. The lender can only seize the pledged shares in case of default.

- Retention of voting and ownership rights: Because the shares are pledged rather than sold, borrowers typically maintain ownership and voting rights.

- Faster than secondary sales: Secondary transactions can take months to complete, requiring company approvals and legal documentation. Equity-backed loans are much faster and can close in weeks.

What Equity-Backed Loans Fail to Solve

- Concentration risk remains: Borrowers still retain most of their wealth tied to the same startup. The single-asset exposure is still a concern.

- Low asset monetization: Low LTV ratios (around 30%2) mean founders must pledge far more equity than the cash they receive. A founder with $10M in shares receives roughly $3M, while the full downside risk remains.1

- High financing costs: High interest rates (up to 15%2) plus additional fees mean the total annual cost can reach approximately 20%.2

- Risk of losing everything: If the value of the pledged shares declines, the borrower may have to pledge additional shares or risk losing the pledged collateral.

- Repayment obligations create pressure: The interest payment obligation creates cash flow pressures. And added stress of losing a large equity position if you default.

Diversification Alternative for the Paper Wealth Problem

Equity-backed loans address liquidity but don’t solve the concentration risk¹⁵. A founder's paper wealth is still tied to a single company's outcome.

A different approach is diversification. More specifically, the ability to receive access to a diversified portfolio of late-stage private technology companies. .

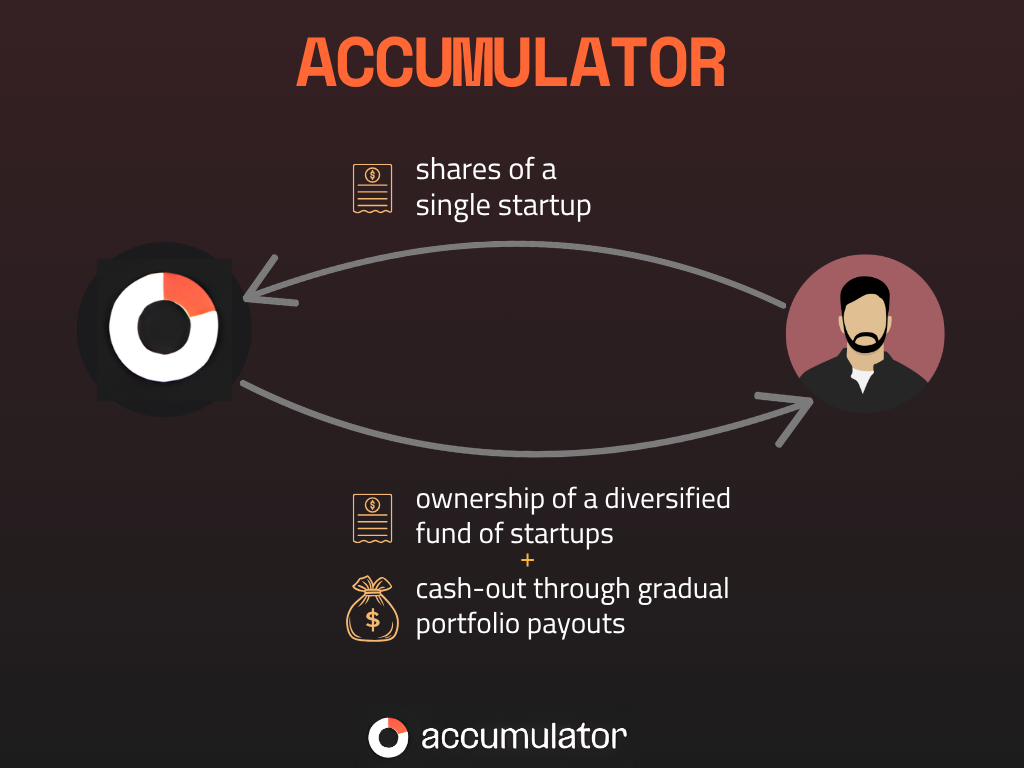

That’s where Accumulator comes in¹⁶.

With Accumulator, founders contribute their shares to a diversified fund holding stakes in multiple late-stage private companies. In return, they receive ownership in the diversified portfolio plus cash liquidity through portfolio payouts7.

Key advantages of this approach:

- Diversified allocation from day one: Concentration risk is reduced immediately.

- Non-compounding fees3: Accumulator does not involve a borrower-level loan repayment obligation, although fund fees, expenses, allocations, and other economic terms apply.

- Liquidity through portfolio payouts: Cash is received gradually if and when portfolio companies exit. There’s no debt involved with repayment obligations.

- Fundraising support: Accumulator provides fundraising support to founders and access to an exclusive community of unicorn-founders4.

When any company in the pool exits, proceeds are distributed to all participants proportionally. The founder benefits not only from their own company's exit but from exits across the entire portfolio.

The founder's problem, at its core, breaks down into two parts: liquidity and diversification.

Accumulator is designed to address both, with liquidity delivered through portfolio distributions, if and when those occur, and diversification achieved from day one8.

Equity-backed loans, by contrast, deliver immediate cash, but unless proceeds are re-invested elsewhere, the borrower may continue to have substantial exposure to the same stock.. And the liquidity part, they do so at a high financing cost and low LTV.

Equity-Backed Loans vs. Accumulator

Here’s the comparison table between these two models:

Bottom line

Equity-backed loans can be useful for founders who need short-term cash. But they also preserve the risk:

- Concentration risk remains fully intact: Most of your net worth stays in a single stock.

- They are expensive: Total annual costs can reach up to 20%2.

- Low LTV: You only access roughly 30%2 of your stock's value.

- You may lose the pledged collateral: A margin call or repayment demand can result in your pledged shares being taken.

For founders who need short-term cash and are comfortable with these trade-offs, equity-backed loans can serve a purpose.

But for those looking to solve the concentration risk, i.e., to reduce single-asset exposure, achieve diversification, and also access portfolio-linked liquidity without debt, Accumulator is one potential alternative for founders seeking diversification..

You get to receive shares in the late-stage private technology companies in exchange for your own shares. You receive ownership in the diversified portfolio plus partial cash liquidity through portfolio payouts. With Accumulator, eligible founders may reduce single-company concentration through exposure to a pooled category-leading private company portfolio, and while receiving payout if and when these liquidity events happen in the portfolio .

Learn more about Accumulator’s approach to private-market diversification here.

Disclaimers:

This material is provided for informational and comparative purposes only and does not constitute investment, legal, tax, accounting, or financial advice, or an offer, solicitation, or recommendation to buy or sell any security or investment product. Any investment with Accumulator is subject to eligibility requirements, definitive legal documents, fees, expenses, risks, conflicts, and other terms described in applicable offering materials. Private company interests are illiquid, difficult to value, and subject to significant risk, including possible loss of value. Diversification may reduce exposure to any single company but does not eliminate risk, prevent losses, or guarantee liquidity, distributions, valuation outcomes, or returns. Accumulator is not a lender and does not provide an upfront cash payment, loan, or advance against private shares. Any liquidity or distributions through Accumulator depend on portfolio performance, timing, expenses, and market conditions and are not guaranteed. Comparisons are illustrative, based on selected assumptions and publicly available information believed current as of the 5th of May 2026, and may not reflect all available market alternatives or current provider terms. Company names are used solely for illustrative comparison purposes. No affiliation, endorsement, or partnership is implied.

1. Loan-based structures vary by provider, borrower, collateral, jurisdiction, documentation, and market conditions. Collateral requirements, advance rates, interest, fees, margin-call mechanics, and lender remedies may differ materially from illustrative examples

2. Numerical examples are illustrative only, not predictions or representations of current provider terms. Actual costs may be lower or higher depending on provider, credit terms, duration, collateral, fees, expenses, and market conditions. Prospective borrowers should verify current terms directly with each provider.

3. Accumulator fee and economic terms vary by transaction size, eligibility, structure, expenses, and applicable documents. Any stated fee should be verified against current offering materials and should not be presented as a maximum unless legally confirmed. 12.5% reflects a fee for a specific eligible volume and is not a maximum fee. Actual fees, expenses, allocations and economic terms may vary and may be higher depending on transaction size.

4. Fundraising support means selective founder/investor network support and introductions where appropriate. No financing, investor participation, or fundraising outcome is guaranteed.

5. “No borrower-level repayment obligation” refers only to the absence of a loan repayment obligation under Accumulator’s model. It does not mean protection from investment losses, valuation declines, illiquidity, tax consequences, fees, expenses, or other risks.

6. Accumulator Cash-out is achieved through gradual portfolio pay-outs which are not guaranteed and depend on performance and market conditions. Any payouts are subject to fund documents, expenses, reserves, timing.

7. Portfolio payouts are not guaranteed and depend on exit timing, portfolio performance, expenses, market conditions, and applicable fund documents.

8. Diversification may reduce exposure to a single company but does not eliminate private-market, valuation, liquidity, tax, or loss risk. Diversification depends on portfolio composition, valuation, expenses, fund terms, and market risks

9. Tax consequences depend on the borrower’s facts, transaction structure, documentation, jurisdiction, and tax advice

Sources:

¹⁰ Heaton & Lucas - Portfolio Choice and Asset Prices: The Importance of Entrepreneurial Risk

¹¹ Hall & Woodward - The Burden of the Nondiversifiable Risk of Entrepreneurship

¹² Moskowitz & Vissing-Jørgensen - The Returns to Entrepreneurial Investment: A Private Equity Premium Puzzle?

¹³ Mayers - Nonmarketable Assets and the Determination of Capital Asset Prices

¹⁴ Markowitz - Portfolio Selection

¹⁵ Hall & Woodward - The Burden of the Nondiversifiable Risk of Entrepreneurship; Heaton & Lucas - Portfolio Choice and Asset Prices: The Importance of Entrepreneurial Risk

¹⁶ CTech on Accumulator’s $46M raise