Secondary Alternatives for Founders

Most founders first deem secondary as the obvious way to access liquidity: sell a small slice of equity, take some cash off the table, and keep building without waiting for an IPO or acquisition.

On the surface, it feels like a clean capital allocation decision. You liquidate your paper money into hard cash by giving up a part of your equity. Your net worth isn’t highly concentrated on a single asset anymore. And you gain personal financial security.

In practice, however, secondary liquidity is rarely frictionless. Transactions are typically priced at a discount to the last round, capital gains taxes reduce net proceeds, investor approvals introduce execution risk, and the legal process consumes more time than most founders anticipate. What looks simple at the headline level becomes structurally expensive once fully unpacked.

For some founders, that tradeoff is rational. For others, it becomes the catalyst to explore secondary alternatives that optimize not just for speed, but for tax efficiency, diversification, and long-term balance sheet strategy.

In this guide, we lay out how secondary works in practice and the other paths founders consider when managing liquidity and risk, including equity pooling and private equity exchange fund structures designed to institutionalize liquidity while preserving long-term upside.

What’s a Secondary Sale? (Secondary Liquidity Explained)

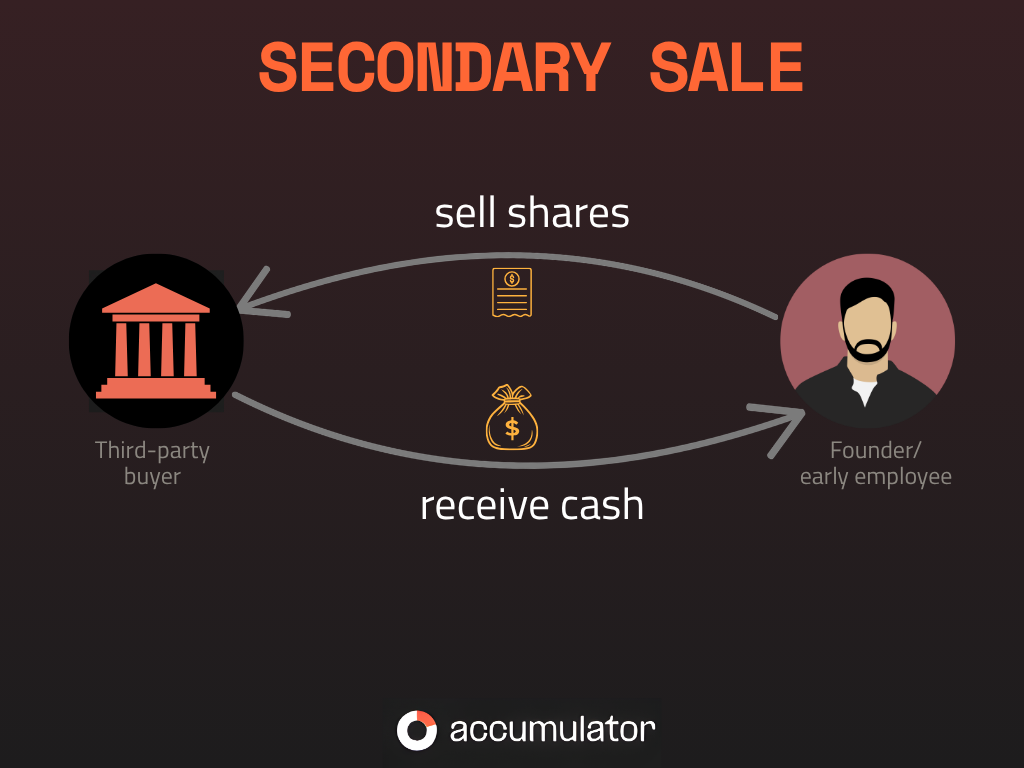

A secondary sale is a private-market transaction in which a founder or early employee sells existing shares in a private company to a third-party new buyer before an IPO or acquisition.

It should not be confused with issuing new shares or raising primary capital. It's actually a personal liquidity event. The company receives no proceeds, and the founder reduces direct ownership in exchange for immediate cash, while the company remains private.

Secondary sales usually happen after a company has raised at least one institutional round and has an externally referenced valuation, creating a price anchor for private transactions. It’s at this point that founders realize the gap between their paper wealth and their personal liquidity.

For example, their company could be worth tens or hundreds of millions on paper, but the founder’s day-to-day finances are still constrained.

For many founders, secondary is the first visible liquidity option. In some cases, it is the right move.

But its true cost: valuation discounts, tax drag, process friction — often becomes clear only during execution.

Secondary should therefore be understood as one liquidity instrument within a broader capital strategy, not the default mechanism for managing founder-level risk and diversification⁴.

Who Needs Secondary Liquidity?

Founders don’t pursue secondary liquidity because they want to “cash out.” They pursue liquidity because their personal financial exposure is disproportionately concentrated in a single, illiquid asset¹ whose value they cannot directly control.

For instance, a founder might own 60–80% of a startup valued at $100 million on paper, yet still be paying themselves a modest salary while the company burns venture capital. Their equity is illiquid, the business is unprofitable, and nearly all of their net worth is tied up in one asset they cannot sell freely². Net worth is concentrated; liquidity is constrained.

Secondary liquidity typically becomes relevant when founders want to:

- Reduce concentration risk by taking some exposure off a single, high-risk asset³

- Create personal financial stability, such as buying a home or building a liquidity cash buffer or de-risking family exposure

- Cover tax obligations triggered by option exercises or other equity events

- Rebalance after years of below-market compensation in exchange for equity upside

- Reduce cognitive load by separating personal financial security from company performance

While founders are the most common users of secondary liquidity, early employees and angel investors sometimes pursue it for similar reasons. The difference is scale. Founders usually hold the largest stakes and feel the liquidity constraint most acutely.

At its core, secondary is a mechanism to partially convert created value into usable capital while remaining fully committed to long-term company building.

The question is not whether liquidity makes sense — it often does — but whether traditional secondary is the most capital-efficient path to achieve it.

How a Secondary Sale Works for Founders

A secondary transaction allows a founder or early employee to sell a portion of their existing shares in a private company to a third-party buyer. That buyer is typically a secondary fund, a private-market platform, or a strategic investor seeking exposure to late-stage private companies.

In practice, a secondary liquidity usually follows a predictable sequence, though rarely a fast one

- Finding a buyer: The seller identifies a buyer willing to purchase private shares. Demand varies widely based on company profile, brand recognition, recent fundraising activity, and overall market conditions. Not every company has an active secondary bid at any given time.

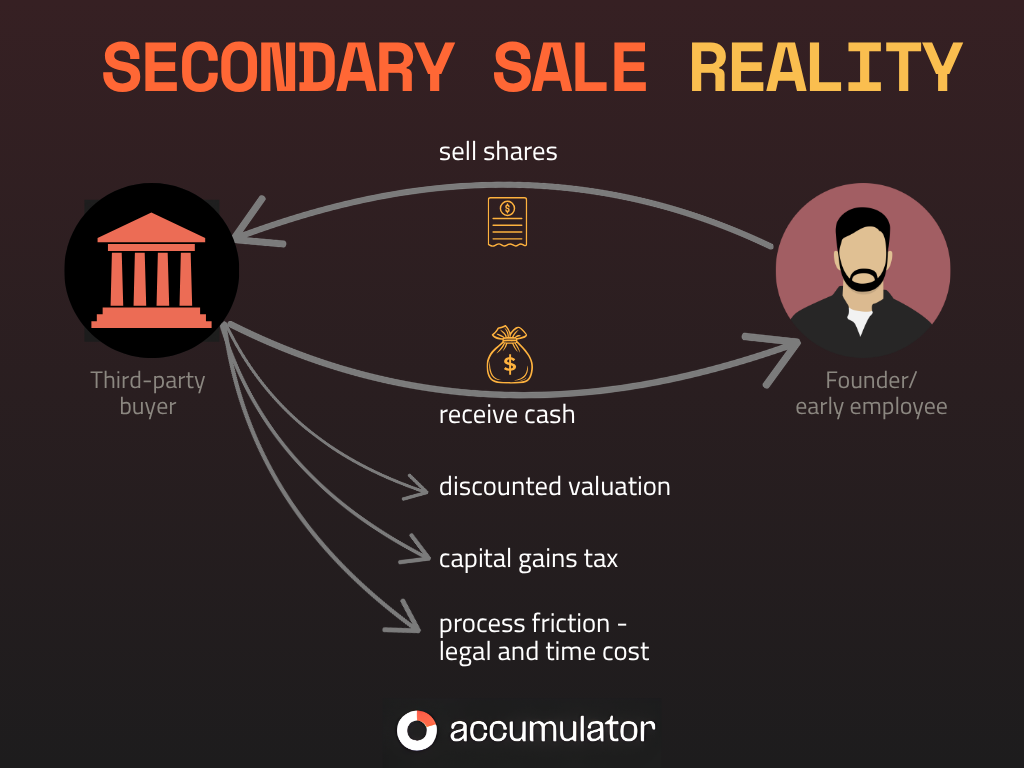

- Agreeing on price: The transaction price is typically set at a discount to the most recent funding round valuation. Discounts of 10–20% are common, and can be higher depending on liquidity, timing, and perceived risk.

- Company and investor approvals: Most venture-backed companies include rights of first refusal (ROFR) and transfer restrictions in their shareholder agreements. The company or existing investors may match or block the transaction. Until those rights clear, no deal is final.

- Legal documentation and closing: Even with alignment, documentation, compliance checks, and administrative reviews can stretch closing timelines into weeks or months. Private liquidity does not move at public-market speed.

- Cash payout and taxes: After closing, the seller receives cash. In most jurisdictions, this is a taxable event that reduces net liquidity. The headline number and the after-tax number are rarely the same.

On paper, secondary looks simple: sell shares, receive cash. In reality, once discounts, tax drag, approval risk, and legal costs are incorporated, it becomes a materially more expensive liquidity instrument than most founders initially model.

Pros and Cons of Secondary

Secondary is often the most visible and straightforward liquidity option available to founders. It can be effective, but it comes with clear tradeoffs that are easy to underestimate at first glance. Below, we list some pros and cons worth considering.

Pros of secondary

- Structural simplicity: You sell shares and receive cash; it’s a direct sale. No derivative overlay, no pooled structure, no forward contract. The mechanics are familiar to most boards and investors.

- Immediate liquidity: Secondary provides cash at closing, not deferred to a future exit event.

- Definitive outcome: Once the transaction closes, the founder has reduced ownership and increased liquidity.

- Broad market familiarity: Many founders, investors, and advisors already understand how secondary works, which can reduce initial hesitation.

- Broad applicability: Secondary can be executed even when a founder does not qualify for more structured secondary alternatives such as equity pooling or private equity exchange fund models.

Cons of secondary

- Discount to valuation: Secondary transactions are typically priced below the latest funding round valuation. The founder absorbs the liquidity discount.

- Taxable event: Selling shares typically triggers capital gains taxes at closing, reducing the net cash a founder actually keeps.

- Approval and process friction: ROFRs and board approvals introduce real deal risk. A negotiated transaction can be matched or declined after terms are agreed.

- Uneven market access: Not every private company has real secondary demand. Liquidity depends heavily on brand, momentum, and recency of the last round.

- Time and cognitive cost: Even “simple” secondary deals can take weeks or months and require ongoing attention during an already demanding period for founders.

- Perceived signaling risk: Even when economically rational, a secondary may be interpreted by investors or employees as reduced conviction. The optics must be managed alongside the economics.

Secondary Alternatives and How to Think About Them

Once founders recognize that a traditional secondary is just one tool, the real question becomes: what are you optimizing for? Speed? Tax efficiency? Diversification? Control? Different secondary alternatives prioritize different constraints. Liquidity for founders is not a single product — it is a capital allocation decision.

The options below are not ranked. The more useful exercise is not memorizing mechanics, but understanding the economic tradeoff each structure introduces.

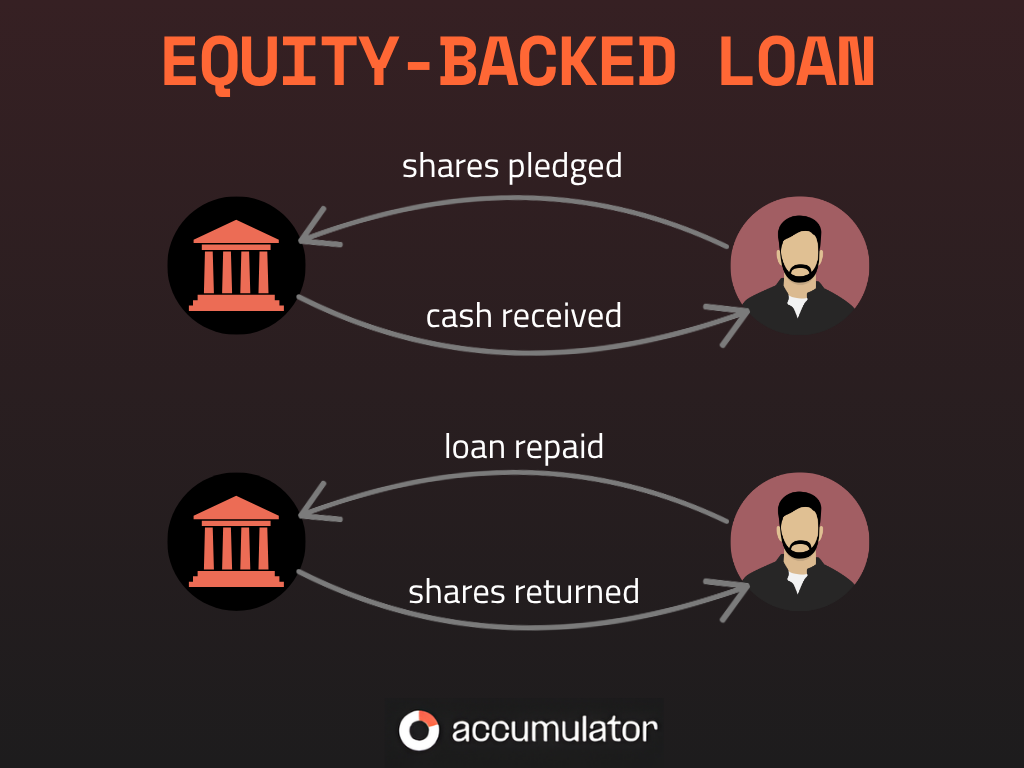

Borrowing against shares (equity-backed loans)

Equity-backed loans allow founders to borrow cash using their startup shares as collateral. The founder does not sell equity outright. Instead, a lender underwrites the value of the shares and provides a loan that must be repaid over time, usually with interest and covenants.

Because private company equity is illiquid and risky from a lender’s perspective⁵, these loans are typically conservative. Loan-to-value ratios are typically low. It is not unusual to pledge $10M of private shares to receive $3M in cash. If repayment obligations are not met, the lender can seize the pledged shares.

Pros

- Structurally simple and familiar to boards and advisors

- Can provide relatively fast liquidity for founders compared to negotiated secondary processes

- Avoids an immediate equity sale

- Typically does not trigger capital gains tax at origination

Cons

- Requires repayment, creating ongoing cash flow pressure

- Interest expense compounds, particularly if liquidity is delayed

- Aggressive collateral terms (such as $3M cash for $10M in shares)

- Risk of losing a large equity position if you default

- Restrictive lender covenants and underwriting

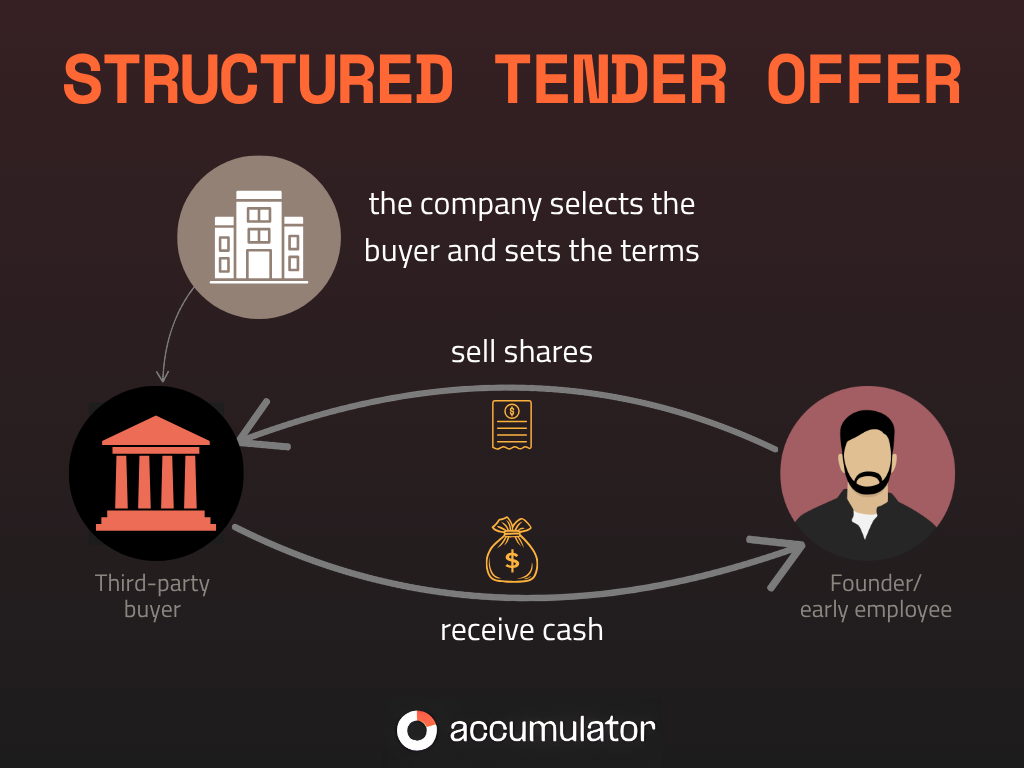

Structured tender offer run by the company

A structured tender offer is a company-led liquidity program that gives founders and employees a controlled opportunity to sell a portion of their shares. Instead of individual shareholders sourcing buyers on their own, the company coordinates the process by selecting approved buyers, setting a price or pricing range, and defining eligibility rules and sale limits.

The offer runs during a fixed window and typically requires board and investor approval. Tender offers provide coordinated liquidity, but founders have limited control over timing, size, and pricing. The company’s capital strategy, not the founder’s personal balance sheet, determines when liquidity occurs.

Pros

- Standardized execution, pricing, and timelines reduce uncertainty

- Centralized process minimizes one-off negotiations and signaling concerns

- Often cleaner execution than ad hoc secondary transactions

- Can provide liquidity to multiple stakeholders simultaneously

Cons

- Founder has no control over when a tender offer occurs

- Pricing, eligibility, and sale size are set by the company

- Liquidity may be limited to a small portion of holdings

- Typically taxable and subject to approvals from investors and the board

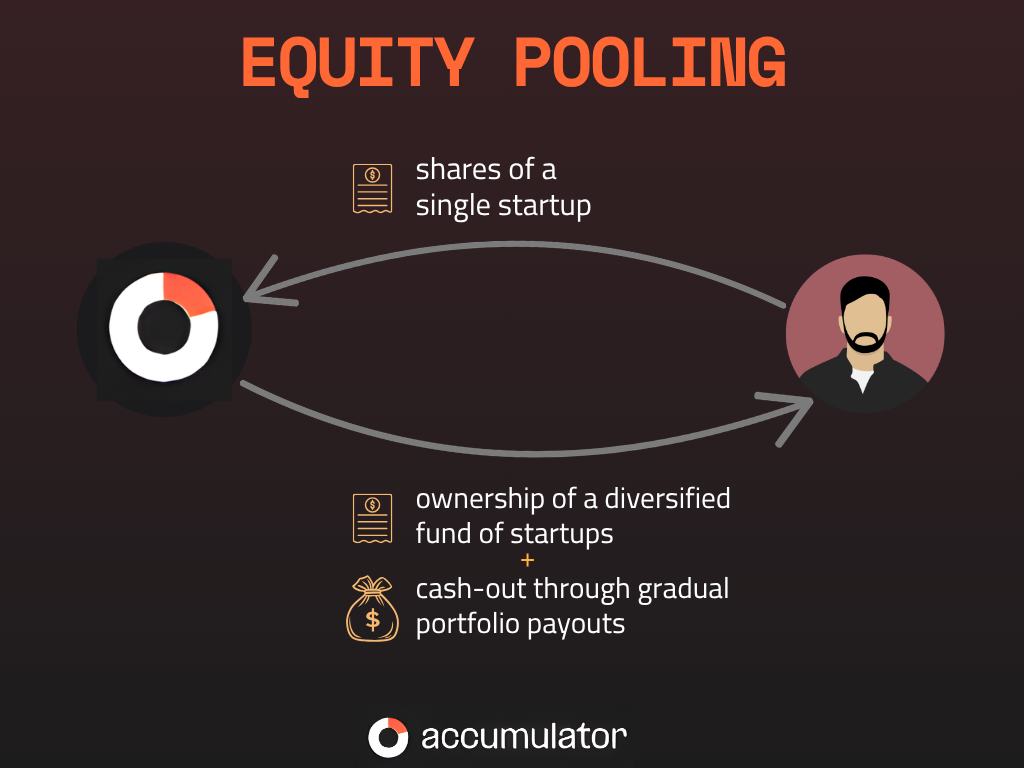

Exchange fund structures

A private equity exchange fund is a structured secondary alternative designed for founders who want liquidity for founders without defaulting to a discounted bilateral sale. Instead of selling shares outright, the founder reallocates exposure through equity pooling.

Rather than negotiating with a single secondary buyer at a liquidity discount, the founder contributes shares into a pooled vehicle. Contribution value is typically referenced to the most recent institutional round, subject to underwriting, eligibility, and fund mechanics.

For example, a founder might contribute a defined percentage of their equity stake, receive a portion of that value as near-term liquidity, and convert the remainder into ownership in the pooled portfolio.

This approach can avoid triggering an immediate taxable sale⁶ because there is no fixed-price equity transfer at the time of the exchange. Founders may obtain near-term liquidity, reduce single-company risk, and gain exposure to a broader venture portfolio. Participants in a private equity exchange fund become economically aligned across the pooled companies, rather than remaining fully exposed to a single operating outcome.

Funds like Accumulator focus on this model specifically for later-stage startups, which is why these structures are usually limited to companies with valuations above $100M and recent institutional rounds.

Pros

- Reduce or avoid the explicit valuation discount

- Immediate diversification across multiple private companies through structured equity pooling.

- Can be structured to defer or avoid immediate tax realization

- No repayment obligation or leverage risk

Cons

- More complex legal and structural setup

- Eligibility limited to later-stage, high-valuation companies

- Requires trust in fund governance, portfolio construction, and valuation

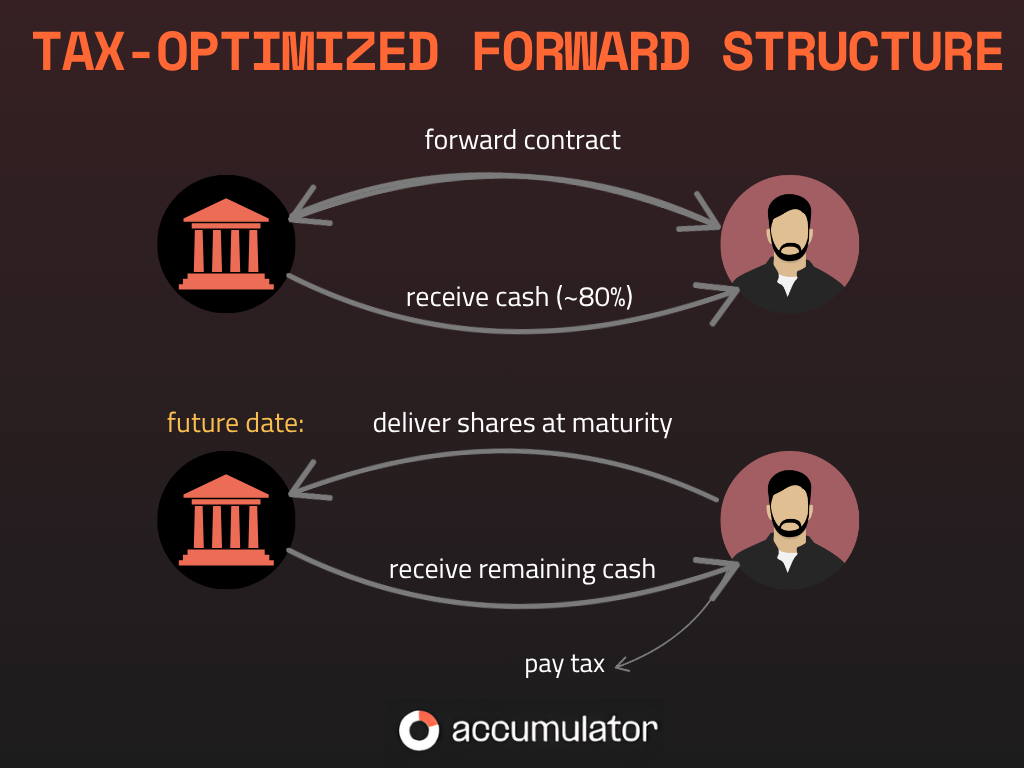

Tax-optimized forward structures

A tax-optimized forward structure uses a variable-price forward contract⁷ instead of a traditional equity sale. This path requires the founder to agree to transfer economic exposure to a portion of their equity. The exact number of shares is typically determined later.

This is an alternative to selling shares at a fixed price today, and it typically occurs during a liquidity event, such as an acquisition or an IPO. And since the price per share is not fixed at the time of the agreement, the transaction can be structured to avoid triggering capital gains taxes upfront.

The objective is to reduce concentration risk and potentially access liquidity without accepting a negotiated discount or triggering immediate tax realization. In practice, these structures are documentation-heavy and require careful tax and regulatory analysis.

Pros

- Designed to avoid immediate capital gains taxes

- No forced valuation discount like a traditional secondary

- Allows founders to address risk earlier

Cons

- Difficult to understand and unfamiliar to most founders

- Heavy legal structure with multiple documents

- Learning curve causes procrastination by founders

- Advisors may slow or kill deals by emphasizing edge-case risks

Doing nothing and delaying liquidity

Doing nothing means the founder keeps their equity unchanged and delays any liquidity decision. There is no transaction, no documentation, and no immediate cost.

This option is often chosen implicitly rather than intentionally, especially when liquidity is not urgent and complexity feels overwhelming. However, time is not neutral. As rounds age, valuations become stale, investor appetite changes, and eligibility for certain structures can quietly disappear.

Pros

- No distraction from running the company

- No taxes or discounts today

- Zero legal or administrative friction

Cons

- Full concentration risk remains

- Financial stress may continue

- Fewer options if liquidity becomes urgent later

- Older rounds can limit future flexibility

Conclusion

Traditional secondary is usually the first liquidity lever founders pull because it is easy to explain: sell shares, receive cash, move on. But once founders look more closely and account for discounts, taxes, approvals, and time, they realize there might be better alternatives out there worth considering.

The alternatives don't necessarily present a perfect structure. They offer trade-offs. Each structure optimizes for a different constraint: speed, diversification, tax timing, control, or simplicity

For instance, equity-backed loans prioritize speed and familiarity but introduce leverage and downside risk. On the other hand, tax-optimized forward structures reduce tax friction and concentration risk but require founders to engage with legal complexity. Exchange funds can offer founders a way to access liquidity while retaining equity exposure and changing concentration, transaction-cost, and tax-timing characteristics. But exchange funds are usually only available to later-stage companies with valuations of $100M or more.

If you do nothing, you choose the most straightforward path, but exposure remains unchanged, while company-led tender offers provide coordination at the cost of individual control.

The right choice depends on what the founder is optimizing for at the moment. What matters most is underwriting the full economic cost of each structure — after tax, after dilution, after risk transfer — before defaulting to the one that feels operationally easiest.

Liquidity for founders is rarely urgent until it is. The founders who make durable decisions treat secondary alternatives the way they treat capital allocation inside their companies: analytically, deliberately, and with a clear view of the trade-offs. That discipline, more than the structure itself, determines the outcome.

DISCLAIMERS

This page is for general informational purposes only and does not constitute investment, legal, tax, accounting, or financial advice. It is not an offer to sell, or a solicitation of an offer to buy, any security or investment product. Any liquidity, diversification, tax, or valuation outcome depends on individual circumstances, company eligibility, fund terms, market conditions, and advice from qualified legal and tax professionals. No transfer, liquidity, distribution, valuation, tax result, investment outcome, or preservation of upside is guaranteed.

Past company valuations, financing rounds, or private-market pricing references may not reflect current fair value or future outcomes. Private company equity is illiquid, speculative, and involves substantial risk, including potential loss of value. Participation in exchange fund, pooling, or structured liquidity arrangements may not result in meaningful liquidity, diversification, tax efficiency, or improved economic outcomes. Founders should consult their own legal, tax, and financial advisors before entering into any transaction. Diversification is subject to portfolio composition, valuation, fund terms, fees, expenses, market conditions, and other risks, and does not eliminate risk or prevent loss.

Sources

¹ Hall & Woodward - The Burden of the Nondiversifiable Risk of Entrepreneurship

² Moskowitz & Vissing-Jørgensen - The Returns to Entrepreneurial Investment

³ Markowitz - Portfolio Selection

⁴ Heaton & Lucas - Portfolio Choice and Asset Prices: The Importance of Entrepreneurial Risk

⁵ Phalippou - Private Equity Laid Bare

⁶ IRS Code Section 721 - nonrecognition of gain/loss on contribution to partnership

⁷ Jagolinzer, Matsunaga & Yeung - An Analysis of Insiders’ Use of Prepaid Variable Forward Transactions